Proflex Market Update - Week 20-24 April, 2026

Record RSI | Mag 7 Gauntlet | FOMC Hold | CTA Positioning

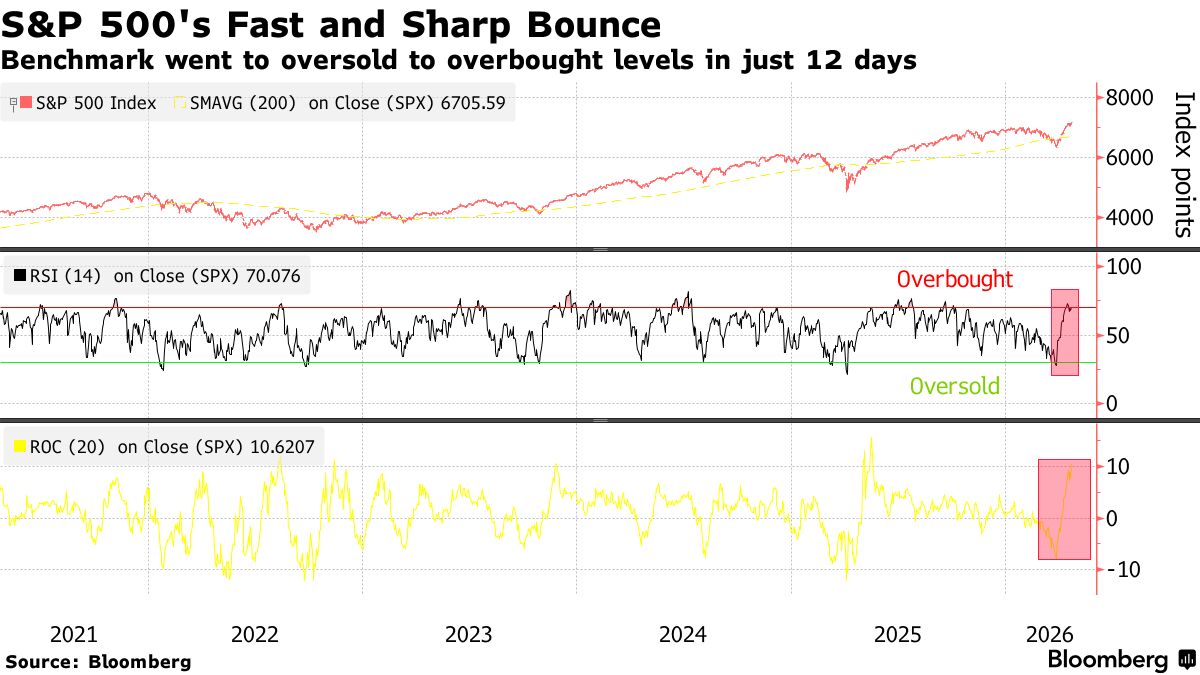

Coming off the J-shape rally we described in Week 17 (a straight-line grind to all-time highs with barely a breath) the market arrives at its most crowded moment in years.

The S&P 500 sits near all-time record highs.

This isn't a garden-variety overbought reading. And yet: Q1 earnings are coming in at a 13.4% net profit margin — the highest FactSet has recorded since it began tracking the series. 84% of reporters are beating estimates, with an average upside surprise of 12.3% versus the five-year norm of 7.3%. The fundamentals are exceptional. This week tests the tension directly. The question this week is whether the next 72 hours validate the overbought multiples or reset it.

|

CTAs, hedge funds, and retail investors all re-entered during April's recovery. There is almost no natural buyer left to push the next leg higher from pure momentum.

But the historical record is clear: after each of the five prior instances when breadth-overbought reached 70%+ over the past 20 years, short-term returns were soggy and then proved to be exceptional buying opportunities in every single case without exception.

As we outlined in Week 11 when triple-witching scaffolding was about to unroll: don't chase any rally until you see how the market absorbs the next structural event. The structural event this week is earnings.

The Earnings Gauntlet: Four Giants, One Evening

Wednesday, April 29 is a moment with no recent precedent. Meta, Microsoft, Alphabet, and Amazon all report after the closing bell a single evening that will determine the valuation case for roughly $8 trillion in market cap simultaneously. Apple follows Thursday.

|

The bar going in is demanding (Expected Financials in Q1 2025):

- Meta: Revenue $55.6B (+31% YoY). Full-year capex $115–135B — the market wants ad revenue acceleration to justify that spend.

- Microsoft: Revenue ~$81.4B (+16% YoY). Azure flagged at ~37% constant currency growth last quarter, capacity-constrained through FY2026 end.

- Alphabet: Revenue ~$107B (+19% YoY). Google Cloud growth rate and AI monetization are the critical variables.

- Amazon: Revenue ~$177B (+14% YoY). AWS trajectory and advertising margin expansion.

The early read from the season is constructive. Tesla beat on EPS ($0.41 vs. $0.37 estimate) and raised full-year capex to $25B+ — a signal of conviction, not contraction.

The broader Q1 blended growth rate is 15.1%, with 84% of reporters beating (See chart) above the five-year average of 78%.

Get This Analysis Every Week

Join 250+ investors at Google, Amazon & Apple who start their week with Proflex.

No spam. Unsubscribe anytime.

The crowded nature of the Wednesday print is itself a risk. If even one of the four misses on guidance: not earnings, but guidance — the selloff will be immediate and hit the entire complex simultaneously. There is no stagger to absorb the shock.

FOMC, PCE, and GDP: Three Prints, One Week

The macro calendar is stacked alongside earnings in a way that rarely happens.

On April 29-30, the Fed holds its FOMC meeting. The CME's Fedwatch tool now shows less than a half cut priced for 2026 (11bps) just around 80% of a cut (20 bps) by the end of next year. The chance of a hike is 10%.

But Powell's press conference matters for a reason beyond rates: his current term ends May 15, 2026. Every word he speaks Wednesday will be filtered through the lens of transition. Markets will parse whether the handover feels orderly or politically managed.

Also on April 30: Q1 2026 GDP (first estimate) and March PCE inflation both release. The Atlanta Fed's GDPNow model is tracking Q1 at 1.2% — well below the 2%+ markets assumed at the year's open. If the GDP print lands at or below 1% alongside PCE still sticky above 3%, the stagflation narrative reignites in real time.

The 10-year sits at 4.33%, the 2-year at 3.81%. Rate cut expectations for 2026 have collapsed to one cut maximum — likely September or October.

CTAs Tapped Out: The Fuel Has Burned

CTAs have largely finished their buying program, hedge funds are de-grossing, and pension rebalancing is about to inject a top decile supply event into the tape.

April's recovery from the Week 16 lows through the J-shape straight to new ATHs was partly driven by $45B in CTA re-deployment (Goldman estimate).

Hedge funds followed, officially turning net long for the first time in two months. QQQ pulled $6.5B in five-day inflows as retail confirmed the move.

The positioning is now stretched long across every systematic and discretionary measure. There is no dry powder in the CTA community.

The key reversal levels Goldman is watching: S&P 6,500. These are the thresholds where CTA models flip from buyers to sellers. The current S&P at 7,162 is 9% above the flip trigger meaningful cushion but earnings-driven selling could close that gap fast.

🔍 What We're Watching

- Wednesday, April 29: Four Mag 7 earnings after close + FOMC decision + Powell press conference — the most information-dense single evening of 2026

- Thursday, April 30: Apple earnings + Q1 GDP (Atlanta Fed tracking 1.2%) + March PCE — watch for stagflation signal if GDP < 1.5%

- CTA reversal thresholds: S&P 6,566 and Nasdaq 24,132 — levels where systematic selling begins

- Breadth: Does the SOX RSI cool through time or through price?

🧭 Proflex Playbook – Discipline in an Information Dense Week

With corporate earnings, War in Intermediation & Insitutional Reversal, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures