Quick Note: We've moved! All future Proflex newsletters will be sent from contact@proflexfinance.com — please add this to your contacts so you never miss an update.

Proflex Market Update - Wk 10

War Shock | Oil Near $100 | S&P Next Support

— Proflex Panel

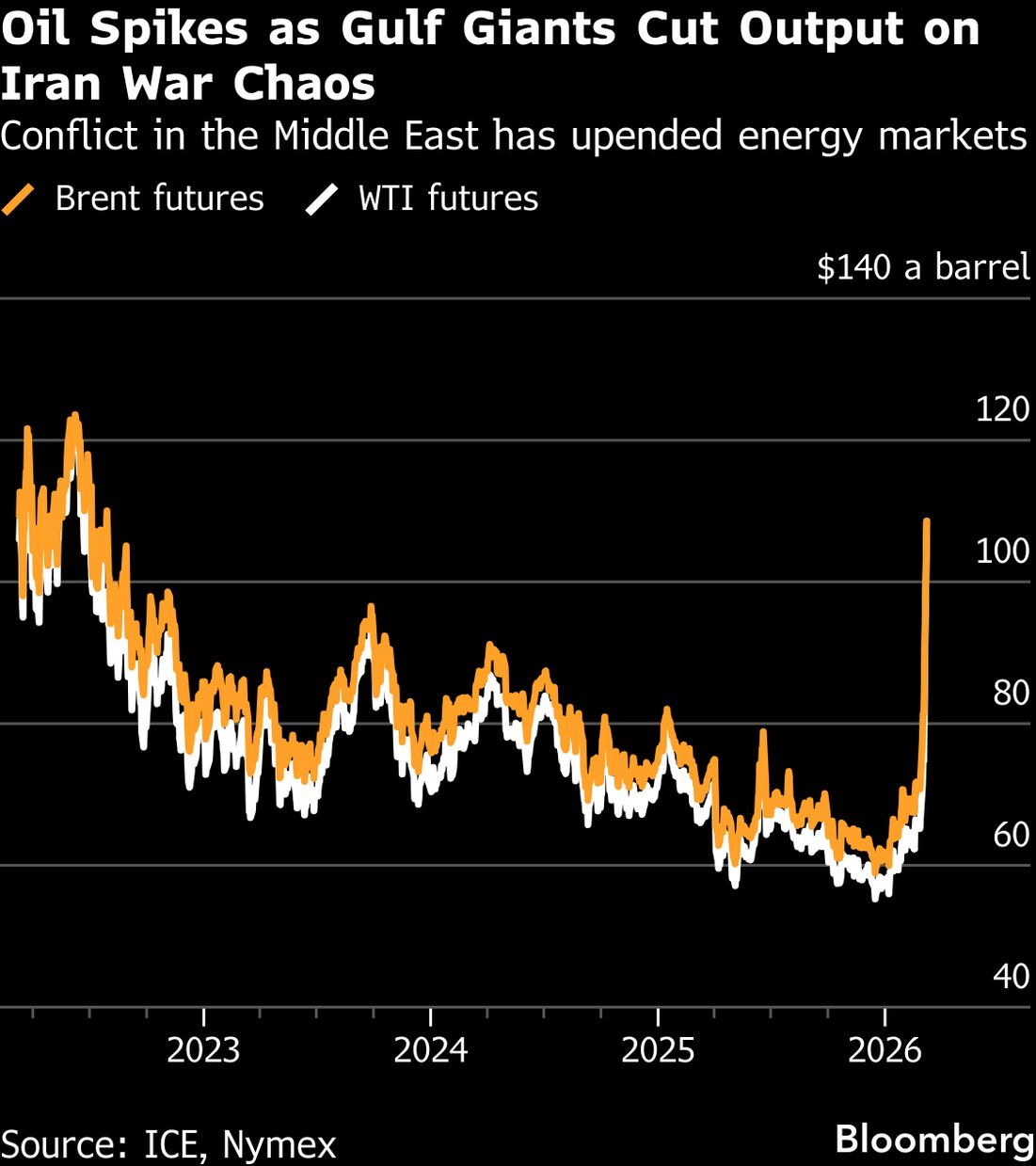

The Iran war has entered its second week, and the market is now in full war-premium mode.

The Strait of Hormuz is effectively closed, Middle Eastern producers are cutting output as storage fills up, and crude oil surged 35% last week — the biggest weekly gain in WTI history.

Meanwhile, $5+ trillion in options exposure is amplifying every move, turning the market into a volatility machine where derivatives are driving price action more than fundamentals. The S&P 500 closed last week down 2%, the Dow shed 3%, and futures opened Monday down another ~1.5% . The question this week is binary: Does the Strait reopen, or does the conflict deepen? Proflex Macro Discussion Group Join our invite-only, expertly moderated WhatsApp group—where macro meets community. Tap into real-time commentary from Proflex experts on market shifts, policy cycles, and global events—alongside daily discussions from 190+ Silicon Valley CTOs, CEOs, family offices, and seasoned HNIs. Proflex Exclusive Investor CommunityKey Drivers This Week |

|

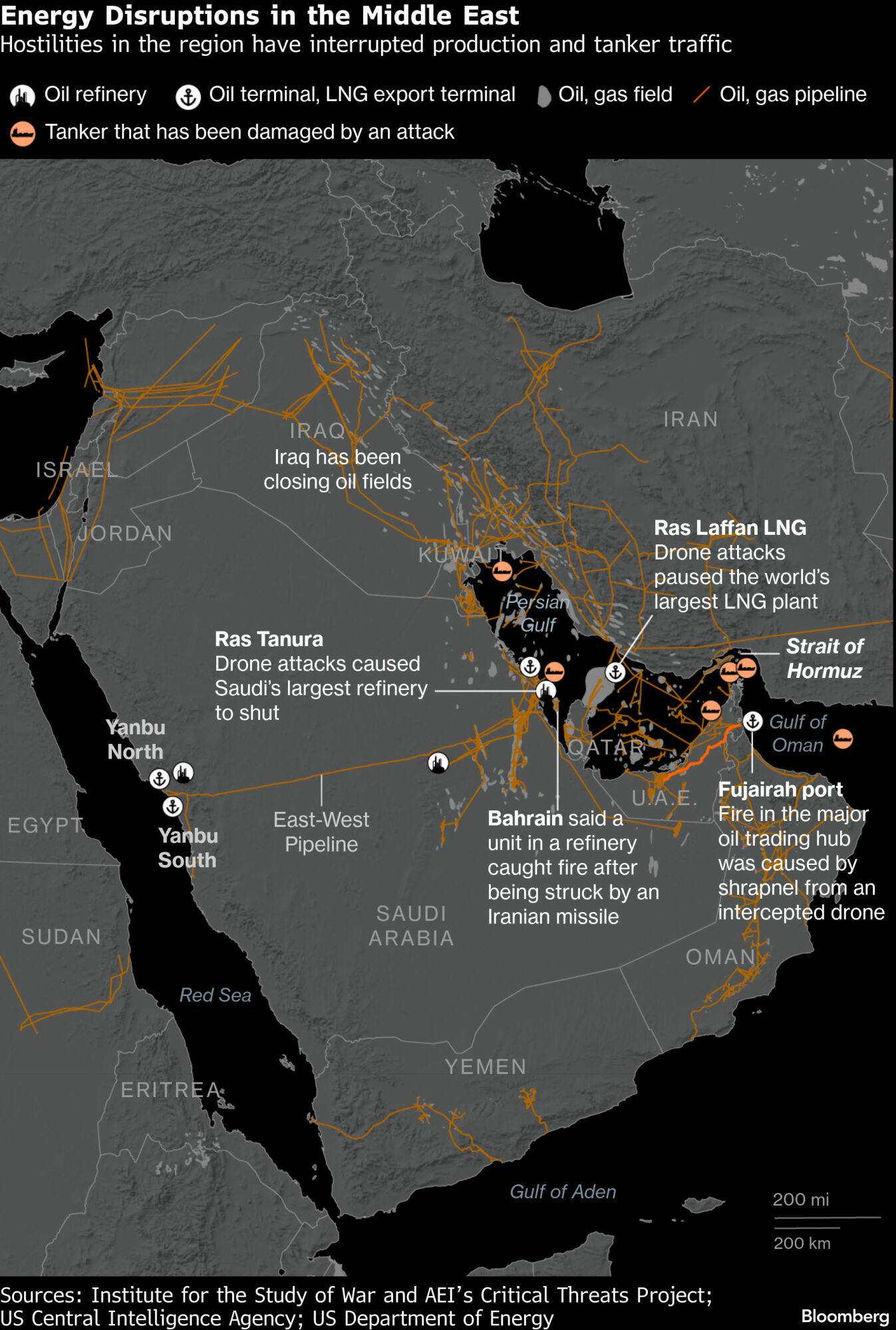

Here's where it gets structural:

- Iraq's production has collapsed 70% — from 4.3M barrels/day to 1.3M — because there's nowhere to store oil that can't ship.

- Kuwait and the UAE are cutting output. Qatar halted LNG production after its facilities were struck.

- JPMorgan estimates production cuts could exceed 4M barrels/day by end of this week if the Strait stays shut.

The derivative products downstream from oil — jet fuel, fertilizer, petrochemicals, LNG are all repricing simultaneously.

This is a supply chain contagion that bleeds into food prices, transport costs, and ultimately CPI.

The Resolution Thesis: Why This May End Sooner Than Markets Fear

The market is currently pricing in a prolonged war and indefinite closure of energy supplies. We believe that overcorrects the actual trajectory.

- War objective redefined: Trump initially talked regime change. Now the focus is nuclear facilities and military infrastructure. Speaker Johnson called it "limited in scope and duration." Mirrors the June 2025 Twelve-Day War pattern.

- Political incentive is massive: Gas prices are a third rail. White House calling this "short-term disruption." Navy escorts ordered for tankers.

- Backchannels active: NYT reported Iranian operatives reaching out on terms. EU gas futures dropped 12% on that headline. Iran's Pezeshkian apologized to Gulf states — clear de-escalation signal.

- Iran weakening: Houthis notably restrained (3 statements in 10 days vs usual aggression). Hezbollah degraded. Iran's retaliatory capability eroding under sustained strikes.

We believe the US is actively working toward a resolution. The war objective has been redefined to nuclear facilities, not regime change, and Trump is already walking back the most extreme rhetoric.

There is too much politically on the line for this to drag on indefinitely. Our belief is that this should start improving soon but we cannot predict exact timelines, and further escalation remains a real tail risk.

SPX Futures & "Triple Witching" volatility on March 20

Get This Analysis Every Week

Join 250+ investors at Google, Amazon & Apple who start their week with Proflex.

No spam. Unsubscribe anytime.

The S&P 500 futures indicate opening around 6,700 on Monday, pressing against critical technical support at 6,700. This is the level the market absolutely must hold this week.

A sustained close below 6,700 would confirm a structural technical breakdown:

- Trading below the 50-day moving average and the February lows

- January's all-time high of 7,008 confirmed as a failed breakout

- Opens the path to 6,500–6,300 — Sep'25 & Nov'25 lows

The options market is acting as an accelerant. With $5 trillion in quarterly derivative exposure, dealer hedging flows amplify moves in both directions — when markets drop, dealers sell to re-hedge, pushing them lower still.

But the flip side is equally powerful. If 6,700 holds and any de-escalation headline emerges — even a single tanker convoy making it through Hormuz safely — those same mechanics snap the market back violently. A V-shaped recovery is entirely on the table if the energy picture shifts.

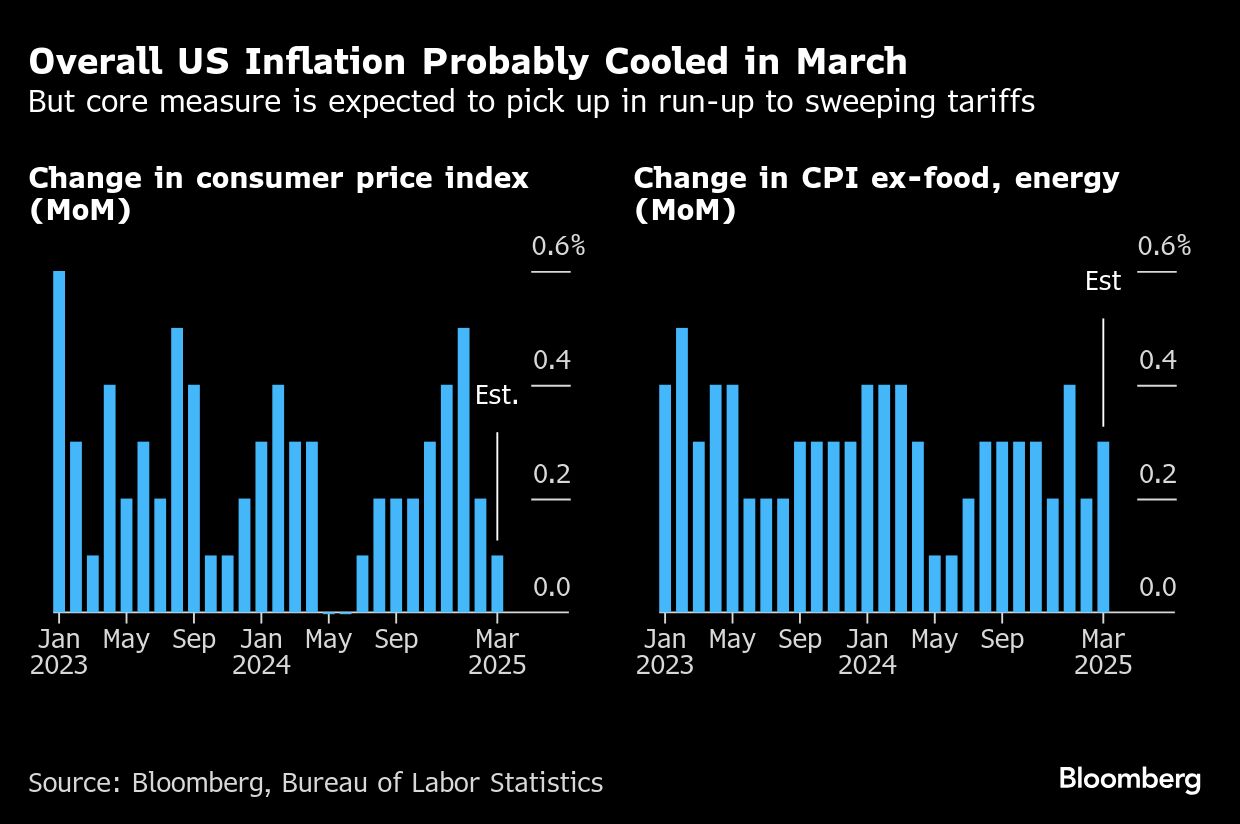

Macro: CPI on Wednesday, Fed meet on March 18

February CPI lands Wednesday — the first inflation reading that will capture the early oil surge. January CPI came in at 2.4% YoY, down from 2.7%. Any upside surprise from energy pass-through would effectively kill remaining rate cut expectations for the first half.

|

The Fed meets March 18 with markets pricing a 90%+ chance of no change at 3.50–3.75%. The oil shock is creating a textbook stagflation setup — rising prices alongside slowing growth — the worst possible environment for policy flexibility. The Fed is boxed in.

Hard Assets & Crypto: Decorrelation Working

Gold has pulled back to ~$5,090 on profit-taking after its extraordinary run (up 65% in 2025). Silver surged above $90/oz on combined safe-haven and industrial demand. Both are performing exactly as hard assets should during a war cycle.

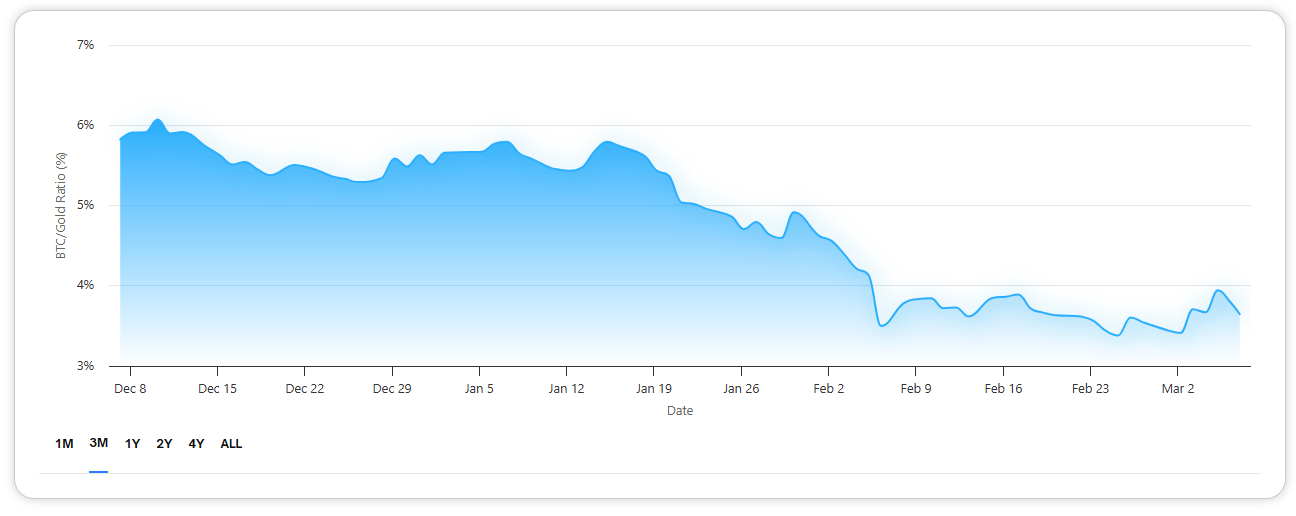

Bitcoin (~$67,500) is the quiet outperformer — holding better than gold on a volatility-adjusted basis this week.

The BTC/Gold ratio is showing bullish divergences, and institutional whales are accumulating (Abu Dhabi's Mubadala added spot BTC ETF exposure in mid-February).

|

🧭 Proflex Playbook – War Premium, Hard Asset Conviction

The market is pricing in the worst case. This is not a time for panic but a time for disciplined positioning.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures