Proflex Market Update - Week 27 April - 1 May, 2026

Earnings Peak | Yield Ceiling | Market Breadth Collapse

The S&P 500 closed last week at 7,230, a fresh all-time high.

Earnings season just delivered the best beat magnitude in recent memory. Mag7 EPS growth is now tracking at +61% for Q1, up from the +22.4% expected at the end of March.

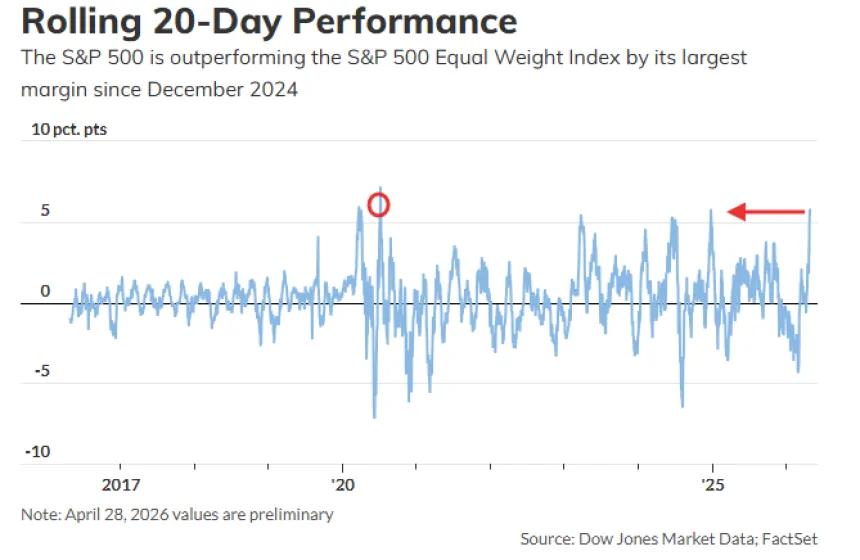

The overall beat magnitude is running at +20.7% above estimates — roughly triple than what was seen in Q4 2026. By every conventional measure, this is an exceptional earnings season. The problem is that the market already knows. The earnings tailwind is behind us now. The Mag-7 has reported. The hyperscalers have reported. Look at what the index is actually doing versus what it appears to be doing. The equal-weight S&P 500 has declined roughly 1% over the same period the cap-weighted index has rallied 14% off its March lows.

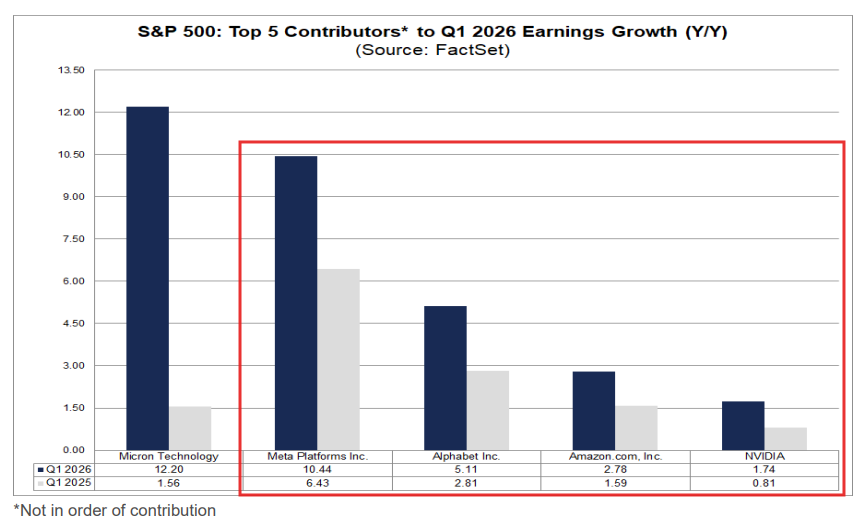

Four names (GOOG, NVDA, META, AMZN) account for four of the top five contributors to S&P earnings growth this quarter. The fifth is Micron. Meanwhile, the Fed just delivered its most divided vote since 1992, holding rates with three members dissenting against the easing bias in the statement.

|

|

Hyperscaler capex confirmed what Proflex has argued since Week 15: the AI infrastructure buildout is not slowing.

Meta committed to $64–72B in 2026 capex. Microsoft guided $80B for the fiscal year. AWS revenue accelerated. The numbers backed the thesis.

|

Here is what changes now.

The fundamental catalyst that drove this rally is effectively running out. The Mag-7 has reported. The beat is in. And the market must now hold these valuations on something other than earnings momentum.

With the 10-year at 4.30% and the Fed signaling no cuts until at least July, equity multiples are being supported by positioning and inertia, not by a broadening fundamental case.

Yields and the Fed: The Ceiling That Will Not Move

The April 29 FOMC meeting was the most divided since 1992. The vote was 8-4. Three members — Hammack, Kashkari, and Logan — dissented against the easing bias. One member, Miran, voted for a 25bp cut.

The message underneath the split: the Fed has no consensus on where it goes next.

The data is making it harder, not easier:

- Core PCE came in at 3.2% annual. Headline PCE at 3.5%. Goolsbee, speaking Saturday, said recent inflation readings were "bad news" and called for "assurance we are going back to 2%."

- The 10-year is at 4.38%, up from 4.30% a month ago. The 30-year is approaching 4.96%. Real yields via TIPS are at 1.88%. All of this tells us that it is not a cheap market

CME FedWatch puts the probability of a hold through June at 89%.

Get This Analysis Every Week

Join 250+ investors at Google, Amazon & Apple who start their week with Proflex.

No spam. Unsubscribe anytime.

|

Kevin Warsh is expected to have his Senate confirmation vote the week of May 11, and the June 16–17 FOMC will likely be his first meeting as Chair.

He arrives with a more hawkish reputation than Powell. April CPI drops May 12 — one day after his likely confirmation. If that print is hot, the narrative around any 2026 cut becomes materially harder to sustain.

The Hollow Rally & Market Breadth Signal

The S&P 500 is at a new all-time high. What is underneath it is not healthy.

- Only 56% of S&P 500 stocks are trading above their 200-day moving average while the index prints new records.

- The equal-weight index has declined roughly 1% over the same period the cap-weight index has rallied 14%. Hedge fund gross leverage sits at 292.8%, near three-year highs (Goldman prime brokerage).

- CTA equity exposure is at the 88th percentile. Goldman CTA deployed approximately $45B into equities during the recovery. Those buyers have largely bought. The marginal buyer at 7,272 is harder to identify.

Goldman equity strategy flagged this directly: this level of breadth concentration has historically preceded larger than average drawdowns over the following six to twelve months.

|

The 14-day RSI showed a textbook negative divergence: price made a new high, RSI made a lower high. That same pattern appeared at the January 2018 top, the February 2020 top, and the late 2021 peak.

What do the next months hold?

Brent is at $108. WTI is at $101. Every $10 of sustained oil feeds 0.2–0.3 percentage points into headline CPI within three months, and a similar amount into core inflation the quarter after.

That pipeline is already running. The April CPI print on May 12 will be the next critical read on how much energy has passed through to broader prices.

Stack everything together, and this is what the summer looks like:

- The worst seasonal window of the year (May through October has averaged 1.7% S&P returns since 1950 versus 7%+ for November through April)

|

- A midterm election year (average peak-to-trough drawdown of ~19% between April and October in midterm years going back to 1962)

- Collapsing breadth, CTA positioning at the 88th percentile, yields that will not fall

And an active geopolitical conflict keeping inflation elevated. None of these forces individually guarantees a correction. Together, they have removed the margin of safety that usually absorbs selling when summer volume dries up.

🔍 What We're Watching

- April CPI on May 12 — the first clean energy passthrough read and the single most important data point for the summer rate cut narrative

- Kevin Warsh Senate confirmation vote (week of May 11) — first Fed chair transition during an active geopolitical conflict in decades; his tone sets the policy frame for the rest of 2026

- Hormuz transit volume — two vessels through on May 4 is a signal, not a resolution. Daily transit counts are the real scoreboard

- Brent above or below $100 — that level marks the line between manageable and stagflationary in the Fed calculus

- Stocks above 200DMA — if that reading drops below 50% while the index holds ATH, the breadth warning becomes structural

🧭 Proflex Playbook – Discipline in an Stretched Rally

With corporate earnings, War in Intermediation & Insitutional Reversal, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures