Proflex Market Update - Week July 6 to July 10, 2026

SK Hynix's $26.5B Blockbuster | Korea's 7th Circuit Breaker | Fed Kills the Easing Bias | Record Treasury Auctions

Two markets looked at the exact same AI-memory story this week and drew opposite conclusions.

In New York, the Dow printed a fresh all-time high on last Monday, the VIX collapsed toward 15-16, and SK Hynix walked onto the Nasdaq and raised $26.5 billion — the largest foreign IPO in US history with the book 7× oversubscribed.

In Seoul, the same names that anchor that HBM trade kept forcing the Korea Exchange to halt trading entirely.

The S&P added ~1.2% and the Nasdaq ~1.3% on the week, led by Meta's +14% run — its best week since early 2024.

|

|

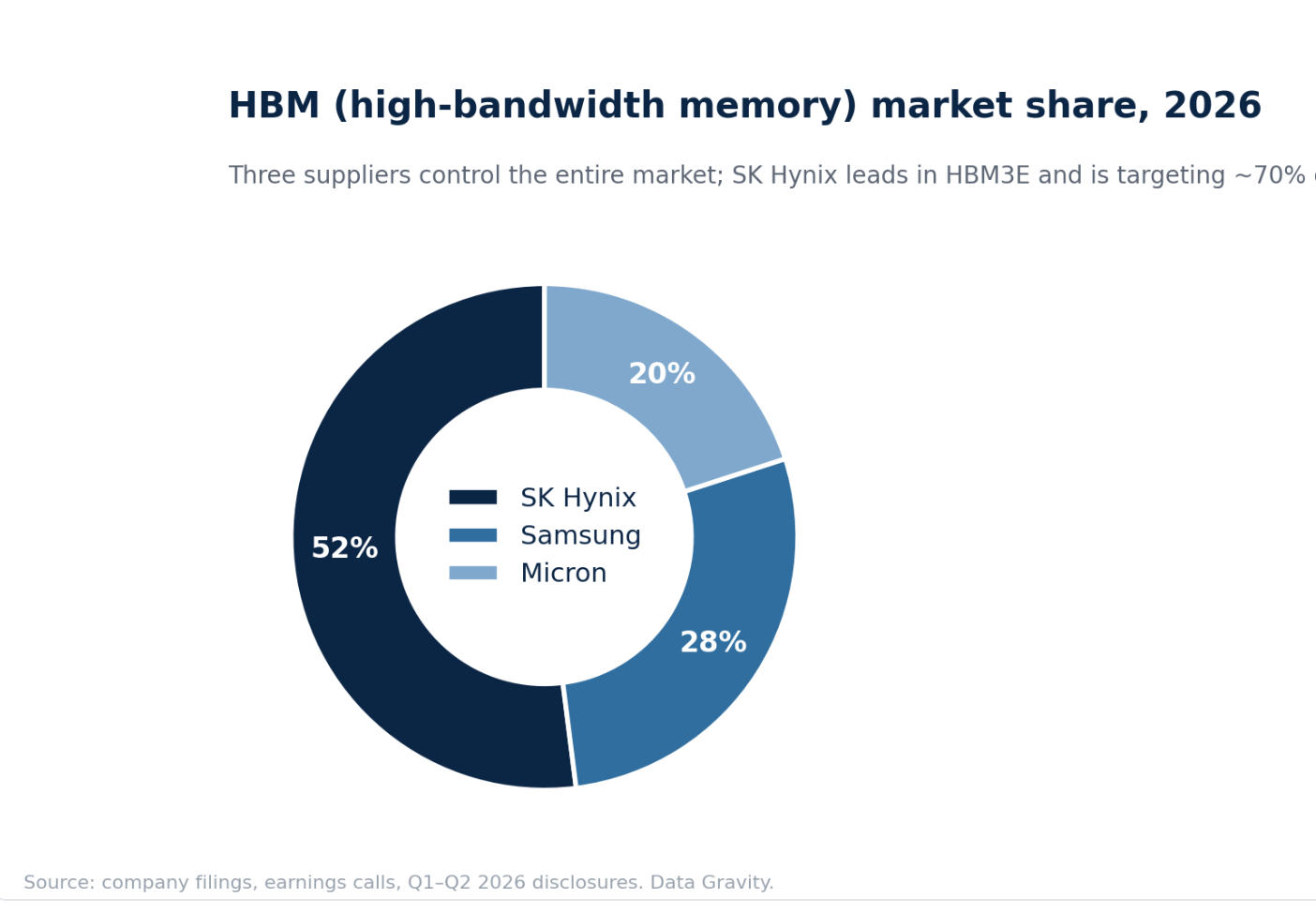

- It locked up the lion's share of next-generation HBM4 orders

- The timing is the tell — a company sells equity when it can get the best price, and institutional money still wants concentrated exposure to the AI-infrastructure buildout, even after a brutal semiconductor tape

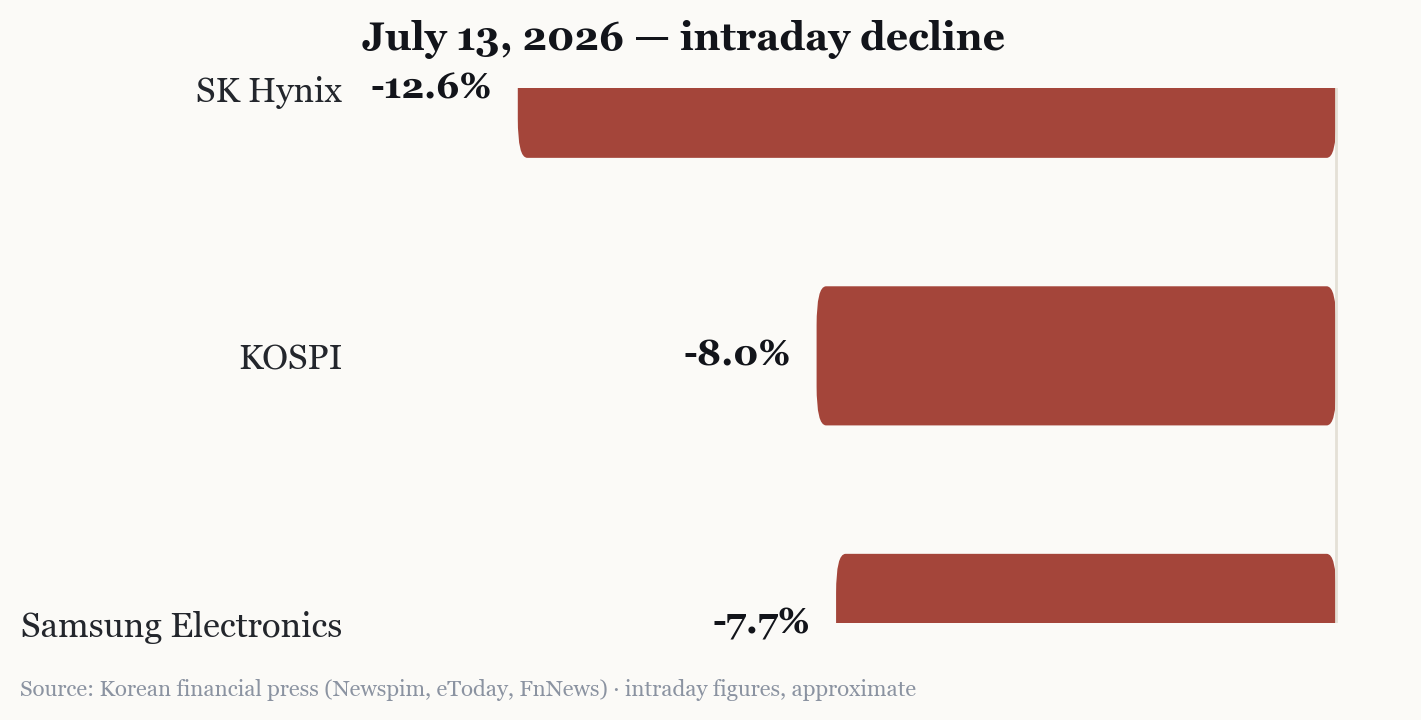

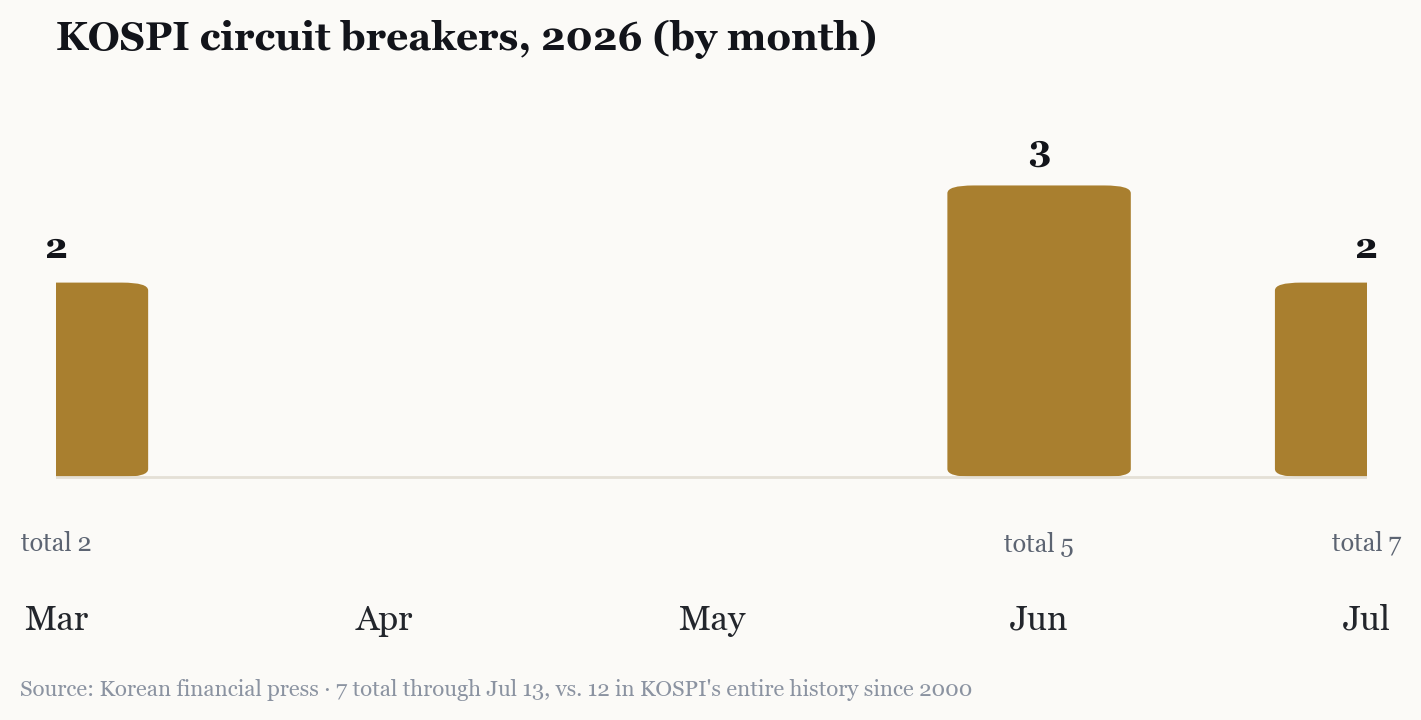

Korea's 7th Circuit Breaker: Where the Same Trade Is Breaking

While New York bought SK Hynix, Seoul kept halting. The KOSPI triggered its 7th circuit breaker of 2026:

|

- A market-wide halt requires an 8% index drop — and has now tripped 34 sidecars in the first half alone, topping the 2008 financial-crisis record

- The index is down roughly 27% from its June peak

- Samsung and SK Hynix account for the bulk of a foreign-investor exodus that hit ~$100 billion in H1

The trigger was expectations, not earnings. Samsung posted a 19-fold jump in operating profit — and it wasn't enough. The bar for anything AI-adjacent has become almost impossible to clear.

The Fed Kills the Easing Bias

The June FOMC minutes (released Jul 8) did the one thing markets weren't positioned for: they removed the easing bias entirely.

- Officials split hawkishly, flagging that firming would be warranted if elevated inflation persists

- Markets now price roughly a coin-flip on a September rate hike — a hike, not a cut — with some tightening more likely than not

- Fed Chair Warsh reinforced it, warning bluntly that "prices are still too high"

|

The awkward part: this hawkish turn lands on top of a 57,000 payroll print and 4.2% unemployment — the labor market is softening while the Fed pivots toward tightening. The policy box is getting smaller.

Get This Analysis Every Week

Join 250+ investors at Google, Amazon & Apple who start their week with Proflex.

No spam. Unsubscribe anytime.

The 30-Year at a 2007 High

The bond market voted with the Fed. This week's auctions cleared cleanly but expensively:

- 3-year at 4.179%

- 10-year at 4.580% (2.59 bid-to-cover)

- 30-year at 5.058% — the highest long-bond yield since 2007

Crucially, the 30-year stopped through, meaning demand actually exceeded expectations at that yield, with indirect (foreign) bidders taking a near-record share.

Oil, Hormuz, and the Weekend That Resets the Week

US–Iran strikes escalated mid-week before drifting back toward negotiations:

- Brent pushed to a ~$79 peak (WTI held under $72), a ~4–5% weekly gain

- Then the weekend broke the truce: renewed strikes, Iran declaring the Strait of Hormuz closed and targeting US facilities across the Gulf

- Tanker traffic data will tell us whether the waterway stays open to commercial traffic — equities are opening this week lower on exactly that, compounded by the Asia-led chip selloff

Notably, hard assets did not act as the hedge:

Proflex Macro Discussion Group

Join our invite-only, expertly moderated WhatsApp group—where macro meets community.

Tap into real-time commentary from Proflex experts on market shifts, policy cycles, and global events—alongside daily discussions from 190+ Silicon Valley CTOs, CEOs, family offices, and seasoned HNIs.

Proflex Exclusive Investor Community- Gold fell ~1.5% and silver ~4% on the week, pressured by the same rate-hike repricing

- Energy (XLE) led the sector board

- Bitcoin quietly added ~6% on the month, once again decorrelating from the metals.

🔍 What We're Watching

- Hormuz traffic — tanker transits are the cleanest read on whether this is a scare or a shock

- Korea's 8th circuit breaker — the canary for whether AI-memory fragility goes global

- TSMC earnings (Jul 16) — the definitive check on real AI demand vs. expectations

- The September Fed path — any further hawkish speak hardens the hike into the base case

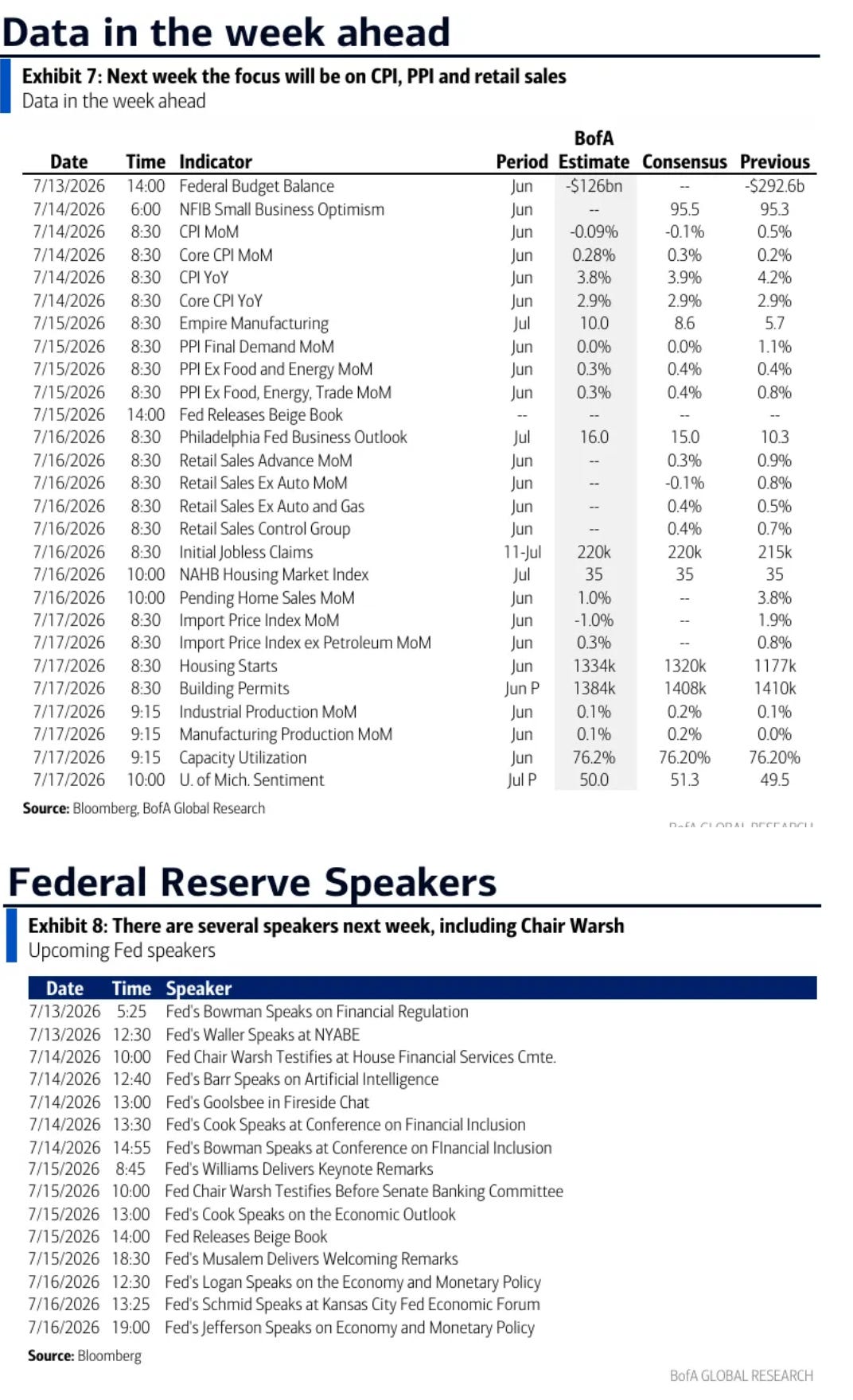

Data in the week ahead:

|

🧭 Proflex Playbook – Discipline in an Stretched Rally

With War in Intermediation, Institutional Reversal, International market selloff, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

| Proflex All-Access Subscription (Yearly) |

| Proflex All-Access Subscription (Monthly) |

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures