Proflex Market Update - Week Jun 22 - Jun 26, 2026

The AI Unwind | Micron’s Record Earnings | Korea’s Circuit Breaker | Strait Fragility

This was the week the AI trade cracked from the inside. Not a macro shock, not a war headline.

A positioning unwind.

Hedge funds dumped US technology at the fastest pace in more than a decade, the Nasdaq 100 logged one of its worst sessions of 2026, and Korea’s Kospi tripped a circuit breaker.

Yet underneath the wreckage, Micron printed the single best quarter in its history. Two narratives collided.

We have been building to this.

|

|

- Semiconductors and semi equipment were net sold for eight straight sessions, more than half the dollar selling.

- Mag 7 stocks were net sold for a fifth consecutive week. Gross and net exposure now sit near three year lows, in the 4th and 6th percentiles.

- The tell: semis positioning is still in the 98th percentile versus five years. The unwind is early, not over.

Alphabet is the poster child.

It raised $84.75 billion in equity, then fell 15% from its $402 May high while losing senior AI talent to OpenAI and Anthropic. Selling felt orderly (asset managers raising cash, no panic), but the bid is gone.

Micron’s Record and the Memory Tax

Micron answered the gloom with a blowout. Fiscal Q3 revenue hit $41.5 billion, a fifth straight record, up 346% year over year, beating by $5.6 billion.

EPS was $25.11 against $20.20 expected. Q4 guidance: roughly $50 billion. The stock cleared $1,200.

CEO Sanjay Mehrotra called memory “the strategic value in the AI era,” backed by about $100 billion in multiyear take or pay contracts.

But the same scarcity that made Micron rich is now a tax on everyone else. Memory pricing is the new inflation:

- DRAM rose 98% in Q1 alone (TrendForce), with another 58% to 63% expected this quarter.

- Apple raised MacBook and iPad prices 18% to 25%. Apple stock fell about 6% on the news.

- Microsoft pushed through a second Xbox price hike inside a year.

Korea’s Circuit Breaker and the Levered ETF Trap

Get This Analysis Every Week

Join 250+ investors at Google, Amazon & Apple who start their week with Proflex.

No spam. Unsubscribe anytime.

The epicenter was Seoul. The Kospi fell 9.99% on Monday, tripping a circuit breaker, then dropped another 5.81% on Friday as Samsung and SK Hynix got hit by chip demand fears and forced deleveraging in single stock leveraged ETFs.

|

South Korea’s ETF closed the week down about 8%.

This landed in the same week as the Russell reconstitution, the largest liquidity event of the year.

The Nasdaq closing cross executed a record $334 billion in 1.6 seconds on June 26. The Russell 1000 close ran at 29.7% of daily volume versus a 16.7% norm.

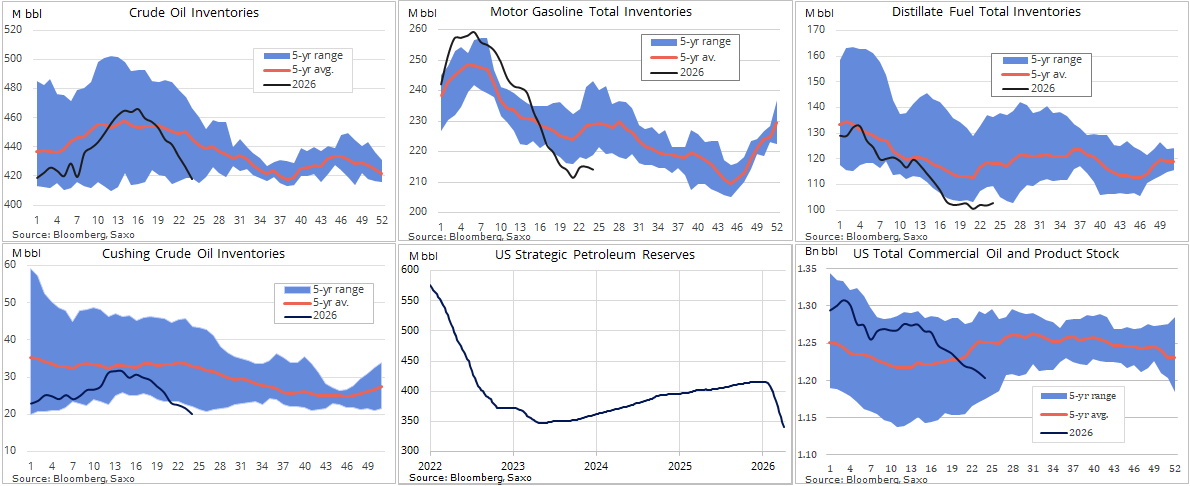

Strait Fragility, Cheaper Oil, and Credit Cracks

The macro backdrop actually eased, which softened the blow.

WTI fell about 9% and the 10 year yield slipped 8 basis points to 4.37%, a tailwind for rate sensitive names.

|

Homebuilders (+9.4%), Healthcare (+8.4%), and Insurance (+6.4%) led as money rotated.

But two cracks opened in credit and crypto:

Proflex Macro Discussion Group

Join our invite-only, expertly moderated WhatsApp group—where macro meets community.

Tap into real-time commentary from Proflex experts on market shifts, policy cycles, and global events—alongside daily discussions from 190+ Silicon Valley CTOs, CEOs, family offices, and seasoned HNIs.

Proflex Exclusive Investor Community- Iran fragility returned. Four party talks in Switzerland nearly collapsed over the weekend (fire traded, talks reported cancelled, Araghchi claiming exclusive control of the Strait) before Axios reported a US and Iran agreement to stop attacking and meet in Qatar on Tuesday. Kalshi odds of the Strait normalizing by September 1 fell from 68% two weeks ago to 46%.

- Risk off hit leverage. Bitcoin slid from $63K to $59.7K. STRC bonds (the leveraged crypto treasury model) traded at junk spreads near record lows. SpaceX bonds widened: the 5y/30y spread moved from 65bp at issue to 83bp, converging with Oracle’s curve.

🔍 What We're Watching

A holiday shortened week, but a heavy one. US markets close Friday July 3.

- June Nonfarm Payrolls land Thursday July 2 (pulled forward from Friday). The single most important print of the week.

- Fed Chair Warsh speaks Wednesday July 1 on a panel at the ECB’s Sintra forum. His first major international stage.

- Manufacturing ISM Wednesday, plus ADP, JOLTS, Challenger cuts, consumer confidence, and factory orders.

Earnings in the Q1 to Q2 gap: NKE, STZ (Tuesday), GIS, FDS (Wednesday).

🧭 Proflex Playbook – Discipline in an Stretched Rally

With War in Intermediation, Institutional Reversal, International market selloff, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

| Proflex All-Access Subscription (Yearly) |

| Proflex All-Access Subscription (Monthly) |

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures