Proflex Market Update - Week Jun 15 - Jun 19, 2026

Record $8.3T Expiry | Warsh's Hawkish Debut | Iran Truce, Reversible | Semis at the Turn

A new Fed chair walked in and told markets the cuts they'd been waiting for aren't coming and stocks fell, then climbed straight back.

Kevin Warsh's first FOMC meeting delivered a hawkish dot plot, the largest options expiration in history rolled off the board, and a fragile Iran truce flickered on and off all week.

That's the tension. VIX sat near 16, Brent eased to ~$80 from its ~$98 conflict peak, and risk appetite looks intact.

|

|

The mechanism matters more than the headline.

A large share of dealer gamma: the positioning that quietly absorbs volatility and keeps dips orderly disappeared with that expiry.

Citadel Securities' Scott Rubner framed the aftermath bluntly: "flows matter more than fundamentals" in the near term, with pension-fund rebalancing converging into the same two-week window.

With the stabilizer gone, the market becomes more sensitive to flows as investors rebuild exposure into month-end.

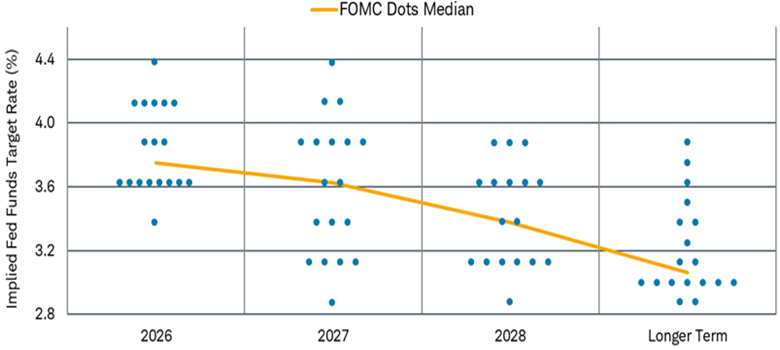

Warsh's Hawkish Debut: The Dot Plot Flips

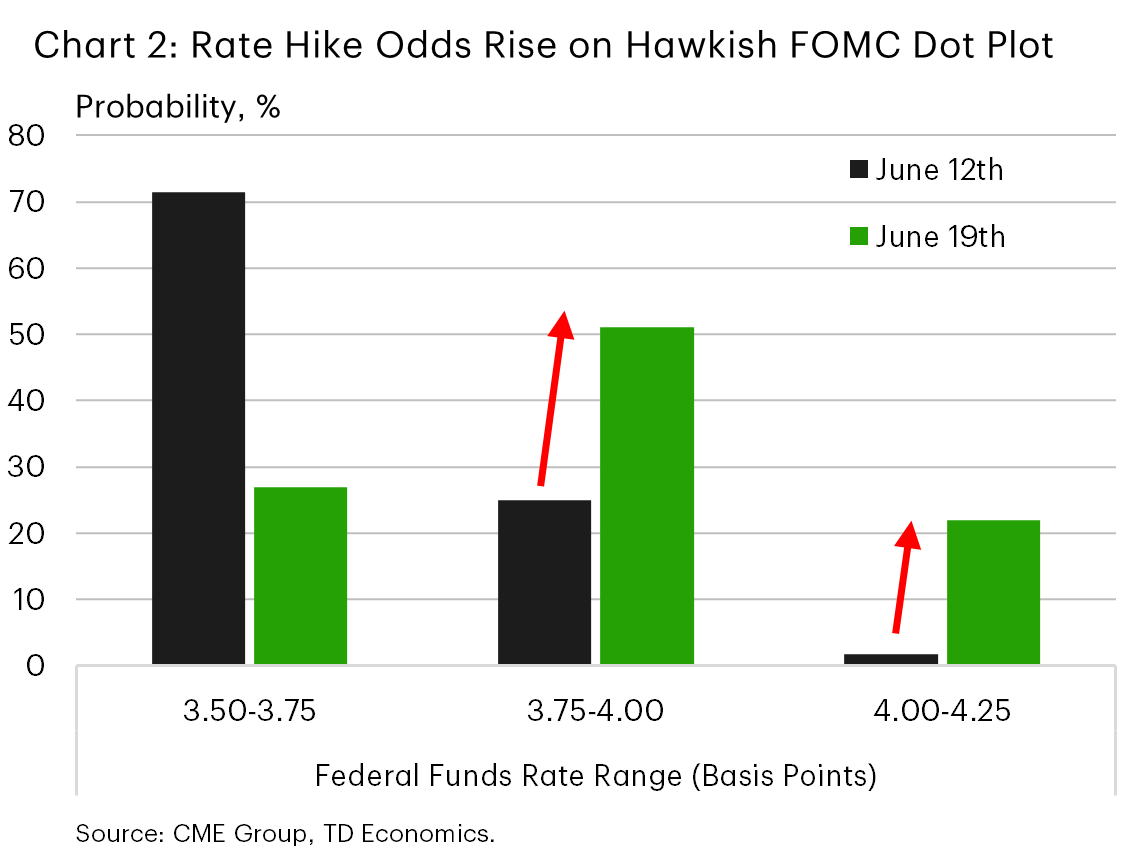

Kevin Warsh chaired his first FOMC meeting on June 17 and held the funds rate at 3.50–3.75% in a unanimous 12–0 vote. The hold was never the story — the dot plot was.

The committee removed its prior easing bias entirely: zero cuts now penciled for 2026 (down from one in March), and 9 of 18 members now project at least one rate hike.

|

Inflation forecasts were revised up to 3.6% headline / 3.3% core, with May CPI already running at 4.2% — the hottest since 2023, driven by the energy shock.

Markets sold off Wednesday, then reversed Thursday as chips and cyclicals carried the tape.

CME FedWatch puts roughly 80% odds on a hold at the July 29 meeting.

|

Warsh is known to favor less Fedspeak than his predecessor but the blackout is over and five officials (Williams, Goolsbee, Waller, Kashkari, Barkin) are on the docket next week.

The Islamabad Truce: Real Peace or a Reversible Headline?

The Islamabad Memorandum of Understanding was signed June 17: a 14-point framework with a 60-day ceasefire, a reopening of the Strait of Hormuz, an end to the US naval blockade, and sanctions relief, brokered by Pakistan with Qatar, Saudi, Turkey and Egypt.

|

By June 21, first-round talks in Switzerland produced a "roadmap to a final deal within 60 days," with VP JD Vance reporting "great progress."

Get This Analysis Every Week

Join 250+ investors at Google, Amazon & Apple who start their week with Proflex.

No spam. Unsubscribe anytime.

Then the cracks.

Lebanon is the fault line: Iran briefly declared the Strait closed again on June 20 over continued Israeli operations, even as its own Foreign Ministry said shipping was "operating normally" (CENTCOM counted 55 transits June 21).

Trump warned he'd "hit Iran very hard again… only harder" if proxies weren't reined in; Israel's Israel Katz said there is "no restriction" on IDF action in southern Lebanon.

We've said for weeks that oil is the real scoreboard and Brent at ~$80, down ~36% from the $98 peak, is voting for resolution. Analysts puts Hormuz normalization by August at ~58%.

Semis: Reversal or Head-Fake?

The chip complex was this week's market: Semis led the Thursday snap-back and dragged the Nasdaq up nearly 2%.

The bid has real fundamentals behind it.

NVIDIA priced a $25 billion bond sale on June 15 its first high-grade offering since 2021 and the book was 3.5x oversubscribed, forcing a raise from the $20B target.

|

That's the bond market funding AI capex at scale.

All eyes now turn to Micron, reporting Wednesday, June 24 — the cleanest read on the memory cycle.

Consensus sits near $19.7B revenue at ~81% gross margins, with DRAM contract pricing reportedly up 58–63% and Goldman pegging the 2026 DRAM supply-demand gap at 4.9%: the widest in 15 years. HBM supply for the year is fully contracted.

Institutional Positioning Into Month-End: BoA's Asymmetric Setup

Proflex Macro Discussion Group

Join our invite-only, expertly moderated WhatsApp group—where macro meets community.

Tap into real-time commentary from Proflex experts on market shifts, policy cycles, and global events—alongside daily discussions from 190+ Silicon Valley CTOs, CEOs, family offices, and seasoned HNIs.

Proflex Exclusive Investor CommunityBeneath the calm tape, the positioning math turned lopsided.

Bank of America's systematic models now see a rebound in CTA exposure but with the upside drained out:

+$13bn of buying in a flat market (down from +$35bn last week)

−$21bn of selling in an "up" market (a flip from +$27bn of buying, as higher vol changes the trigger), and −$95bn of selling in a "down" market (vs −$98bn).

Translation: the firepower that would chase a rally has shrunk, while the selling that would hit a decline barely budged. The downside stays asymmetric.

That collides with a dense calendar.

May PCE: the Fed's traditional preferred inflation gauge — lands Thursday, June 25, alongside final Q1 GDP, May durable goods and jobless claims, with June flash PMIs, UMich sentiment and new-home sales rounding out the week.

Treasury auctions 2-, 5- and 7-year notes Tuesday through Thursday, and FedEx (Jun 23) plus the Fed's bank stress-test results add to the load.

🔍 What We're Watching

- Micron earnings (Wed, Jun 24): The memory-cycle confirmation or the leadership trap

- May PCE (Thu, Jun 25): Does the Fed's hawkish pivot get validated by the data

- Hormuz / Lebanon de-confliction: The variable that keeps the truce alive or breaks it

- First post-expiry sessions: How the tape trades with the gamma floor gone

🧭 Proflex Playbook – Discipline in an Stretched Rally

With War in Intermediation, Institutional Reversal, International market selloff, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

| Proflex All-Access Subscription (Yearly) |

| Proflex All-Access Subscription (Monthly) |

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures